A housing policy shift with consequences beyond the mortgage market

South Korea is preparing to tighten the screws on a group that has long played an outsized role in its property market: people who own more than one home. Beginning April 17, authorities are set to restrict the ability of multi-home owners to simply roll over existing mortgage loans when those loans mature, a move that could affect roughly 12,000 cases, according to local media estimates. On paper, the policy sounds technical, even narrow. In practice, it could ripple through home sales, rental supply and household finances in one of the world’s most watched real estate markets.

For American readers, the closest comparison might be a rule change that prevents highly leveraged small landlords from routinely refinancing or extending property loans under the same assumptions that prevailed during years of easy money. But South Korea’s housing system is different in ways that matter. This is a country where housing has been both a basic need and a dominant wealth-building strategy for households, and where a distinctive rental system known as “jeonse” has historically allowed landlords and tenants to operate under financial arrangements unfamiliar to most Americans.

That is why a mortgage rollover restriction aimed at investors could quickly become a story about renters, newlyweds and first-time buyers. Policymakers say the objective is clear: discourage excessive leverage, reduce financial risk and make it harder for investors to accumulate multiple homes by leaning heavily on debt. The uncertainty lies in how the market adapts. Owners under pressure may sell. They may also try to raise cash another way — by changing rental terms, asking for more monthly rent, or exiting the jeonse system altogether.

The stakes are especially high because South Korea’s housing market does not move neatly in one direction. A rule that cools speculative ownership can also squeeze rental supply. A measure that produces more listings for sale can simultaneously increase monthly housing costs for tenants. In that sense, what happens after April 17 will not just test one regulation. It will test whether the government can curb debt-fueled property investing without shifting the burden onto renters already struggling with affordability.

Why the rule matters to Korea’s multi-home owners

At the center of the change is the practice of maturity extension. Until now, many borrowers with mortgages tied to homes they own have been able to reach the end of a loan term and extend it rather than repay the balance in full. For multi-home owners, that flexibility has been a critical part of the holding strategy. It allowed them to sit on properties, absorb interest costs and wait for values to rise, even when rental income alone was not enough to comfortably support the debt.

Restricting that option changes the math. Even if interest rates themselves are not the only burden, the looming possibility of repayment pressure can force owners to reorganize their finances fast. Some may have enough cash or other assets to pay down balances, refinance through different channels, or reshuffle their portfolios. Others may not. Those borrowers could face a more immediate choice: sell a home, convert a rental arrangement to generate more monthly income, or accept higher financial strain.

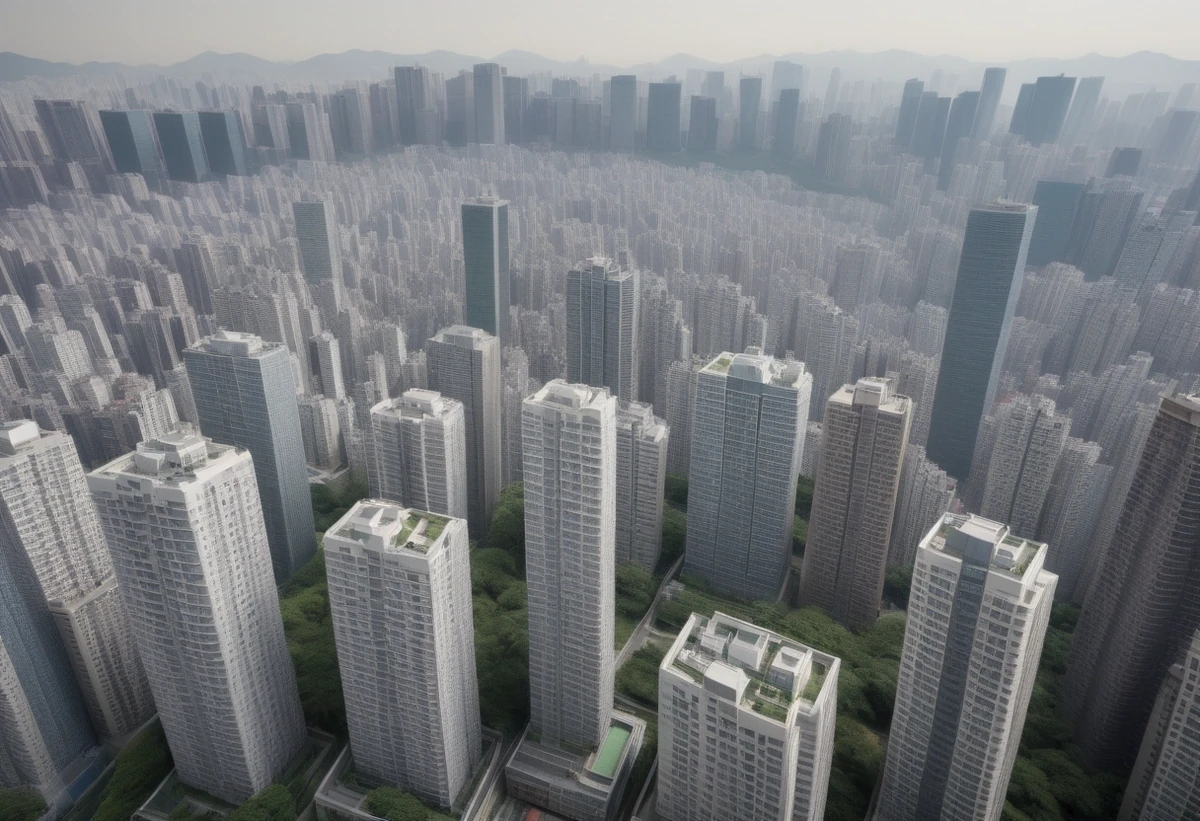

In the United States, policymakers often talk about “mom-and-pop landlords” and institutional investors as distinct groups. South Korea has its own spectrum, but the term “multi-home owner” carries political and economic weight. It often refers to households that own two or more properties, sometimes as a retirement strategy, sometimes as an investment bet, and sometimes as part of a broader culture in which real estate has long been seen as a reliable path to preserve and grow wealth. In Seoul and surrounding areas, where supply is tight and prices have been a central issue in national politics, that ownership pattern has drawn scrutiny for years.

The government’s argument is straightforward: repeated extensions can amount to a long-term debt structure that blunts the discipline loans are supposed to impose. If borrowers can indefinitely carry debt while relying on appreciation or tenant deposits to hold property, authorities see a risk not only to market stability but to the financial system. Tightening rollover rules is designed to force a clearer reckoning with leverage.

Still, housing markets rarely respond in tidy ways. Owners who feel squeezed do not all behave alike. Wealthier investors may absorb the shock with little drama. Those operating on thinner margins may react quickly, particularly if several loan maturities cluster around the same period. That is why analysts are less focused on the raw number of affected loans than on who holds them, how stretched those borrowers are, and where their properties are located.

The Korean rental system Americans need to understand

To understand why renters are so nervous, it helps to understand jeonse, the uniquely Korean lease structure that has no exact American equivalent. Under a traditional jeonse contract, a tenant pays a very large lump-sum deposit to the landlord at the start of the lease and then pays little or no monthly rent. The landlord returns the deposit at the end of the contract. Historically, landlords could use that deposit as a kind of financing source — investing it, using it to support cash flow, or combining it with bank loans to manage multiple properties.

For Americans, the easiest reference point is to imagine a rental market where, instead of first month’s rent and a security deposit, a tenant hands over a sum large enough to resemble a down payment on a home, and then lives rent-free for the lease term. That may sound unusual, but in South Korea it has long been a major pillar of the housing ecosystem, especially for families trying to minimize monthly housing costs and for landlords looking to fund property holdings efficiently.

Over the past several years, however, jeonse has already been under strain. Rising rates, shifting regulations and market volatility have pushed more landlords toward monthly rent or “ban-jeonse,” a hybrid arrangement that combines a smaller deposit with monthly payments. The latest mortgage restriction could accelerate that trend. If landlords can no longer rely on extending debt, maintaining a high-deposit, low-cash-flow lease may become harder. Monthly rent, by contrast, provides regular income that can help service debt or rebuild liquidity.

That is why local reporting has raised concerns about a reduction in jeonse supply. The fear is not merely psychological. It is rooted in the way many landlords have historically assembled their financing: tenant deposits here, mortgage borrowing there, and property appreciation as the long-term payoff. If one leg of that structure weakens, especially the ability to carry debt forward, landlords may move to a model that generates steadier cash each month.

For tenants, that shift can be painful. A family nearing lease renewal may discover that the same apartment is no longer available under jeonse terms, or that a renewal now requires monthly payments that were not part of the original deal. Young workers, newly married couples and households without the savings to buy a home are especially exposed. In a market where wages do not always keep pace with housing costs, even a modest increase in monthly rent can change household budgets in a hurry.

Will April bring a wave of bargain listings?

Some market watchers expect April could bring more “distress sales,” the kind of listings that appear when owners need cash quickly and are willing to cut prices to move a property. That possibility has attracted attention because distressed inventory can shape public psychology even when the broader market does not collapse. A handful of discounted transactions in a neighborhood can become a new benchmark for buyers, putting pressure on other sellers to negotiate.

But a jump in listings is not the same thing as a broad housing downturn. Even the estimate of 12,000 affected loans does not mean 12,000 homes will hit the market. Some borrowers will find workarounds. Some will sell only their weakest-performing assets. Others may lower their asking price without accepting deep discounts. In areas with resilient demand, buyers may absorb fresh inventory without a dramatic drop in values.

That nuance matters. South Korea’s property market is highly regional, much like the United States. A rule that bites hard in one district or city may barely register in another. Homes in investor-heavy areas, especially lower- to mid-priced apartments or villas that were more likely to be bought as rental investments, may feel the pressure first. Prime properties in sought-after neighborhoods may not move much at all, especially if owners there have stronger balance sheets.

There is also the question of financing on the buyer side. In any market, distressed sellers need capable buyers to translate lower prices into actual transactions. If would-be owner-occupants still face tight borrowing conditions or high debt-servicing burdens, a rise in listings may produce more negotiation but not necessarily a surge in completed sales. In other words, price softening does not automatically create liquidity.

For shoppers hoping for sweeping bargains, that could be a reality check. The properties that come up first may not be the most desirable homes in the best locations. Instead, they may be units with weaker fundamentals — less convenient transit access, older building stock, or less attractive layouts — where owners feel pressure sooner. That could limit how much the wider public experiences the policy as a buying opportunity.

Landlords, tenants and would-be buyers are reading the policy very differently

The coming weeks are likely to reveal just how differently the main players in Korea’s housing market interpret the same policy. For landlords, especially those who built portfolios using leverage, the issue is cost management. If the strategy has been to hold homes for appreciation rather than strong rental income, losing the easy option of maturity extension can be destabilizing. Owners with ample cash can adapt. Those without it may have to choose between sale and a tougher lease structure for tenants.

For renters, the biggest concern is not the technical regulation but the practical result at renewal time. If landlords switch from jeonse to monthly rent, households that once avoided recurring housing payments may suddenly face them. If landlords sell, tenants may worry about whether their lease will be honored smoothly and whether their housing stability will suffer. In a country where housing costs are already a major source of anxiety, this is not a small adjustment. It touches everyday life, family planning and consumer spending.

Would-be owner-occupants, meanwhile, see both possibility and risk. A more negotiable market could open doors for households that have been priced out. But only households with a credible financing plan are likely to benefit. This is not a free lunch. A lower asking price helps only if a buyer can secure the loan, handle the down payment and service the debt over time. That means the winners, if there are winners, may be less the broad mass of waiting buyers than the narrower group already positioned to act.

These competing perspectives help explain why housing policy in South Korea often becomes politically charged. Measures designed to curb speculation can be applauded in principle while criticized in practice if they raise rent burdens. Landlords argue that tighter rules can reduce supply and ultimately hurt tenants. Tenant advocates counter that investors have already benefited from a system that encouraged multiple-home ownership and price inflation. Potential buyers tend to support anything that may soften prices, but only as long as financing conditions do not cancel out the benefit.

In short, the same regulation can look like overdue discipline, an unfair burden or a long-awaited opening, depending on where a household stands in the market.

The policy goal is clear. The side effects may be harder to control.

From the government’s perspective, the rationale behind the crackdown is not hard to understand. South Korea has spent years wrestling with elevated household debt, volatile housing sentiment and public frustration over affordability. Restricting maturity extensions for leveraged multi-home owners fits into a broader effort to discourage the accumulation of housing assets through borrowed money and to reduce risk in mortgage lending.

In principle, that is a defensible goal. If authorities can make speculative holding less attractive, they may reduce some of the forces that have pushed housing beyond the reach of many younger Koreans. They may also strengthen the credibility of the lending system by making loan terms matter more at the point of maturity.

But housing regulations often create second-order effects. A policy aimed at stabilizing the purchase market can unsettle the rental market. A measure designed to force deleveraging can prompt landlords to seek cash from tenants instead. This is especially true in Korea, where the same property can sit at the intersection of debt, deposits and investment expectations.

Speed is another issue. When market participants feel a policy is arriving quickly, they often focus first on avoidance and damage control rather than orderly adjustment. Owners may rush to sell before conditions worsen, or revise lease terms aggressively to preserve liquidity. Those individual decisions, multiplied across thousands of households, can shape the broader mood of the market even if the underlying numbers do not point to a crisis.

That is why policymakers will likely be judged on two fronts at once. Did the measure actually reduce the kind of leveraged multi-home ownership it was meant to target? And did it do so without worsening the squeeze on renters through shrinking jeonse supply and rising monthly rent? If the answer to the first question is yes but the second is no, the political payoff could be limited.

The numbers to watch after April 17

The most important data point in the immediate aftermath will be whether home listings actually increase in a meaningful way. A visible rise in supply, especially in investor-heavy areas, would suggest that some owners are choosing or being forced to sell. But listings alone will not tell the full story. Analysts will need to look at completed transaction prices to see whether sellers are truly conceding discounts or simply testing the market.

The second number to watch is the mix of rental contracts. If jeonse listings fall while monthly rent and hybrid leases increase, that would confirm one of the biggest concerns surrounding the policy: that pressure on leveraged landlords is being transmitted to tenants. A gradual conversion is already underway in parts of Korea, but a sharper post-April shift would suggest the new mortgage rules are accelerating the trend.

Third, regional variation will be crucial. The effects are unlikely to be national in a uniform sense. Areas with a high concentration of multi-home owners and significant supply of small apartments or villas used as rentals may see the change sooner and more intensely. Neighborhoods dominated by owner-occupiers may experience relatively little disruption. That distinction will matter for understanding whether the policy is reshaping the market structurally or merely causing localized stress.

Finally, the response of actual end-users — ordinary households trying to rent or buy a place to live — will determine how this story is remembered. If first-time buyers gain negotiating power and renters see little additional strain, officials may claim a policy success. If instead tenants face fewer jeonse options, higher monthly housing costs and little relief on purchase prices, the measure could come to symbolize the difficulty of fixing one part of Korea’s housing market without destabilizing another.

For now, South Korea is entering a familiar but delicate phase in housing policy: the gap between regulatory intent and lived experience. What begins as a technical change in mortgage treatment for multi-home owners may soon be felt in moving decisions, lease renewals and household budgets across the country. That is why this April rule change matters far beyond a narrow slice of borrowers. It is shaping up as a test of whether one of Asia’s most closely watched housing markets can be cooled at the top without turning up the heat on everyone else.

0 Comments