A South Korean chip giant arrives on Nasdaq with a strong first impression

SK hynix, one of South Korea’s flagship semiconductor companies and a critical supplier to the global artificial intelligence boom, made its U.S. market debut on Nasdaq through American depositary receipts, or ADRs, and drew an enthusiastic early response from investors. The company’s ADRs finished their first trading day at $168.49, more than 13% above the offering price, after opening at $170 and climbing as high as $177 intraday.

On paper, the move looks like a straightforward capital-markets story: a foreign company lists securities in the United States, broadens its investor base and gets a new stage on which to tell its growth story. But for American readers, the significance runs deeper. SK hynix is not just another overseas issuer seeking visibility on Wall Street. It is one of the world’s most important memory chipmakers, a company operating at the center of a strategic industry that now sits at the crossroads of U.S.-China rivalry, industrial policy, national security and the race to build the hardware behind AI.

The first-day pop does not, by itself, prove long-term value. Debut trading can be volatile, and companies often see enthusiasm surge or fade once the opening excitement passes. Still, the strong start signals something important: U.S. investors are paying close attention to a Korean semiconductor company that many ordinary American consumers may not know by name, even though its products help power the data centers, smartphones, laptops and servers behind modern digital life.

For years, Americans have mostly encountered South Korean global brands through cars, TVs, smartphones and pop culture. Samsung is familiar. Hyundai and Kia are household names. So are K-pop acts like BTS and Blackpink, and Korean dramas on Netflix. SK hynix is different. It is not a consumer-facing celebrity brand. It is an industrial powerhouse whose importance is easier to understand by comparing it to companies such as Micron, Nvidia’s suppliers or the contract manufacturers and component giants that quietly make the modern tech economy possible.

That is what makes the Nasdaq debut notable. It opens a more direct channel between one of South Korea’s most strategically valuable companies and the deepest pool of capital in the world. It also invites American investors to weigh not only SK hynix’s earnings and technology, but its place in the rapidly changing political economy of semiconductors.

What an ADR listing means for American investors

For many U.S. readers, ADRs can sound like an obscure piece of Wall Street plumbing. In practice, they are a relatively simple mechanism that allows investors in the United States to buy shares tied to a foreign company without having to trade directly on an overseas exchange. Instead of opening an account in Seoul, navigating a different settlement system and trading in Korean won, American investors can buy SK hynix ADRs during U.S. market hours through the market infrastructure they already use.

That matters because ease of access often drives investor participation. A company can be globally important, but if it is difficult for large U.S. institutions or individual investors to buy, it may remain outside many portfolios. By listing ADRs on Nasdaq, SK hynix lowers that barrier. The result is not merely symbolic prestige. It means more direct exposure to American capital, broader analyst attention and a better platform for regular communication with U.S. shareholders.

It also means greater scrutiny. A U.S. listing can enhance a company’s profile, but it can also intensify questions about governance, strategy, capital spending and geopolitical risk. For SK hynix, that may be especially relevant. Semiconductor investors today are not simply asking whether a company can sell more chips next quarter. They are asking whether it can secure supply chains, maintain technological leadership, navigate export controls, manage giant capital expenditures and align itself with the industrial priorities of Washington and allied governments.

On the first day of trading, investors appeared willing to reward SK hynix for its positioning. The company is widely seen as a major beneficiary of demand for high-bandwidth memory, the specialized memory used alongside advanced AI chips. That is a niche with outsized importance at a time when AI infrastructure spending has transformed the semiconductor sector from a cyclical industry story into one of the defining investment themes of the decade.

So while the stock’s opening-day gain may look like a routine headline about a successful market debut, it also reflects a broader reality: U.S. investors increasingly want direct ways to participate in companies beyond Silicon Valley that are crucial to the AI supply chain. SK hynix now has a seat at that table in New York trading hours.

Why SK hynix matters far beyond South Korea

To understand why this listing drew attention, it helps to understand SK hynix’s place in the semiconductor ecosystem. South Korea is a global memory-chip superpower, and SK hynix is one of the pillars of that status. Along with Samsung Electronics and the U.S.-based Micron, it sits in a small circle of companies capable of producing advanced memory at massive scale.

Memory chips do not always capture public imagination the way cutting-edge AI processors do, but they are indispensable. If Nvidia’s graphics processing units are the engines of today’s AI boom, advanced memory is part of the fuel system. It enables the speed and bandwidth required for training and running large AI models. In that sense, SK hynix occupies a position that is less glamorous than consumer electronics branding but potentially just as consequential for the future of computing.

That helps explain why Wall Street, Washington and major tech companies are watching Korean chipmakers so closely. In the American imagination, semiconductors were once often associated with Intel, Silicon Valley innovation and later with Taiwan’s rise as the world’s indispensable manufacturing hub through TSMC. But the reality is broader and more international. South Korea is not a side player in this story. It is one of the central countries in the global chip order.

In South Korea, that role carries national significance. Major conglomerates known as chaebol — family-influenced business groups that have shaped the country’s industrial rise since the postwar era — remain dominant forces in sectors from electronics to autos to shipbuilding. SK Group, the parent conglomerate of SK hynix, is one of those giants. For an American audience, the closest comparison is not a perfect one, but think of a hybrid of a Fortune 100 industrial empire and a national strategic champion, with influence extending across multiple sectors and deep importance to the country’s economic identity.

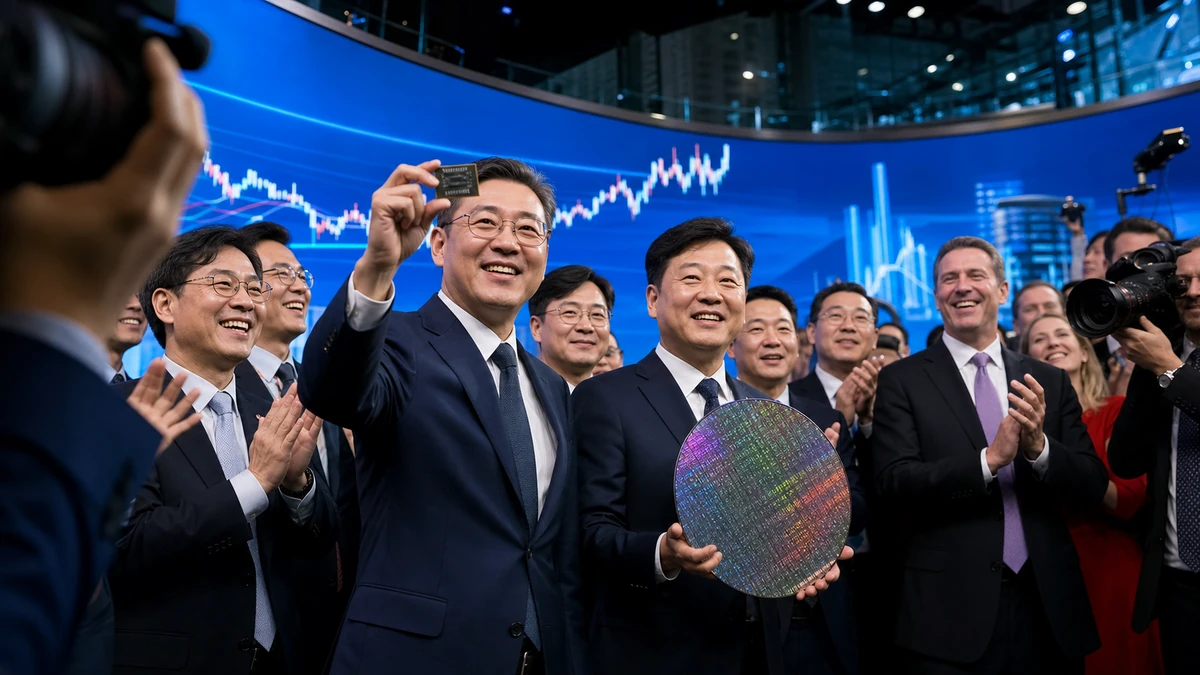

That is part of what made the Nasdaq opening bell ceremony meaningful. Top executives, including SK Group Chairman Chey Tae-won and SK hynix CEO Kwak Noh-jung, were on hand, underscoring that this was not a routine financial transaction. It was presented as a milestone in how a Korean industrial heavyweight wants to be seen — not just as a domestic leader or an Asian exporter, but as a global company engaging American investors directly at a moment when chips have become a central policy issue in the United States.

The listing arrives as Washington pushes for more chipmaking in America

The timing of SK hynix’s U.S. market debut is impossible to separate from the political climate surrounding semiconductor manufacturing. The United States has spent the past several years trying to rebuild domestic chip production capacity, driven by lessons from pandemic-era supply chain disruptions, intensifying competition with China and bipartisan concern that too much critical manufacturing sits outside U.S. borders.

The policy expression of that effort is the CHIPS and Science Act and a broader political push to bring more fabrication, packaging and supply-chain investment onto American soil. Washington has courted not only U.S. companies but also foreign champions from allied countries, especially in East Asia, where much of the world’s semiconductor manufacturing expertise is concentrated.

Against that backdrop, SK hynix’s indication that it is leaving open the possibility of investing in U.S. semiconductor production facilities drew particular attention. The available information does not point to a finalized factory plan, a selected site or a defined investment size. That distinction matters. There is a big difference between saying a company is considering a U.S. production presence and saying it has committed billions of dollars to build one.

But even opening the door publicly is strategically significant. In the current climate, companies are often evaluated not only for their products and profits but for where they build, where they source and how closely their footprint aligns with U.S. policy priorities. By signaling that a U.S. production option remains on the table, SK hynix is acknowledging the direction of travel in global industrial policy.

That does not mean the decision would be simple. Semiconductor fabs are among the most expensive industrial facilities in the world. They take years to plan and build, require highly specialized workforces and infrastructure, and involve enormous long-term bets on technology cycles and customer demand. For SK hynix, any major U.S. manufacturing investment would have to be weighed against its existing and planned footprint in South Korea, where it already has deep operational roots, supplier networks and strategic clustering advantages.

Still, Washington’s interest is clear. U.S. officials have been vocal about wanting more semiconductor investment from global players, including South Korean firms. For American policymakers, attracting companies like SK hynix is about more than jobs. It is about resilience, supply security and ensuring that next-generation technologies are supported by trusted manufacturing bases in allied countries and, ideally, within the United States itself.

Balancing U.S. pressure with massive investments at home in South Korea

One reason the question of a potential U.S. facility is so complicated is that SK hynix is already deeply engaged in major domestic investment plans inside South Korea. The company has recently outlined large-scale projects tied to areas such as Yongin, Cheongju and the Honam region, all part of a broader national push to strengthen Korea’s semiconductor production network.

For Americans unfamiliar with the geography or policy context, Yongin has become shorthand for one of South Korea’s most ambitious chip-cluster plans — an effort to concentrate manufacturing, suppliers, infrastructure and talent in a way somewhat analogous to how U.S. policymakers talk about building advanced industrial ecosystems rather than isolated factories. The idea is that semiconductors thrive not just because one plant exists, but because an entire regional web of suppliers, engineers, power capacity, water systems, logistics and research support develops around it.

That means SK hynix is not choosing in a vacuum between Korea and America. It is managing a far more complex equation: how to preserve and expand its domestic manufacturing base while responding to growing expectations from the United States, one of its most important markets and the center of global capital formation. In practical terms, that may require a mix of strategies, including keeping core manufacturing strength in South Korea, building selected operations abroad and using listings like the Nasdaq ADR to communicate that strategy directly to investors.

For South Korea, this balancing act carries national stakes. Semiconductors are not just another export industry. They are a backbone of the country’s economy and a source of geopolitical leverage. Any major outward shift of production can become politically sensitive at home, particularly if it raises concerns about jobs, regional investment or long-term industrial capacity. At the same time, Korean companies cannot ignore U.S. expectations when American policy, customer relationships and financial markets are so central to the industry’s future.

This is one reason coverage of Korean business stories often requires more context for American audiences than a straight translation would provide. In the United States, debates over industrial policy are frequently framed around bringing manufacturing back from overseas. In South Korea, the issue can look different: how to remain indispensable in a strategic industry while adapting to a world in which allies are also competitors for investment. SK hynix is operating in both realities at once.

A financial debut, but also a branding moment for Korean industry

SK hynix’s successful first trading day was also a branding event, though not in the consumer-marketing sense Americans might associate with a flashy tech product launch. It was a statement that a Korean semiconductor company wants broader recognition in one of the world’s most influential capital markets.

That is important because visibility shapes valuation, partnerships and policy standing. Many Americans know South Korea through culture first. The Korean Wave, often referred to by the Korean term Hallyu, has transformed the country’s image abroad over the past two decades through music, television, film, beauty products and cuisine. Oscar-winning films, sold-out stadium tours and the spread of Korean food from Los Angeles to small-town malls have given South Korea a new level of soft power in the United States.

But the country’s industrial power can sometimes be less visible to general audiences than its cultural influence. South Korea is one of the world’s advanced manufacturing success stories, with global reach in chips, batteries, shipbuilding, autos and displays. What SK hynix’s Nasdaq entrance does, in a sense, is put another part of that Korean story in front of American eyes — not through entertainment or lifestyle branding, but through the machinery of global finance.

There is also symbolic weight in the fact that American investors can now evaluate SK hynix more directly in their own market environment. A company’s technology roadmap, capital expenditures and production plans are no longer being filtered only through foreign-market distance. They become part of the daily U.S. market conversation. That may help elevate SK hynix’s profile among fund managers, analysts and policymakers who track semiconductors closely but have historically focused more on U.S. names and a handful of better-known foreign peers.

The strong first-day performance suggests there is appetite for that story. Investors did not treat the ADR as a novelty. They treated it as a relevant entry point into one of the most consequential sectors in the global economy. That distinction matters for South Korean industry more broadly. It reinforces the idea that Korean corporate champions can seek not only export success in the United States but a fuller presence in its financial and strategic debates.

What investors will watch next

After a splashy debut, the harder part begins. One day of trading can create momentum, but it cannot settle the questions that will define SK hynix’s longer-term relationship with U.S. investors. Those questions are likely to center on several themes.

First is whether enthusiasm around AI-related demand can translate into durable earnings power. Semiconductor history is full of booms and corrections, and memory has been one of the industry’s more cyclical segments. Investors will want to know whether SK hynix can sustain pricing power, preserve margins and maintain technological leadership as competitors respond.

Second is capital discipline. The chip business rewards scale and punishes missteps. Any discussion of new U.S. production, especially if it evolves into a formal project, will invite scrutiny over cost, timeline, subsidies, customer commitments and the relationship to the company’s Korean operations. American markets tend to reward growth stories, but they also expect management teams to articulate clearly why massive spending will generate returns.

Third is geopolitics. Semiconductor companies now operate in an environment where export restrictions, alliance politics and national-security considerations can alter commercial assumptions quickly. For SK hynix, being more visible to U.S. investors may bring valuation benefits, but it also means living more directly under the spotlight of America’s strategic priorities.

And fourth is communication. A Nasdaq listing creates a more regular expectation of engagement with U.S. shareholders, analysts and media. That can be an advantage if management tells a coherent story about AI, manufacturing strategy and global growth. It can also become a challenge if expectations outpace execution or if strategic ambiguity on issues like U.S. production persists for too long.

For now, the most concrete fact is straightforward: SK hynix entered Nasdaq successfully, and the market response on day one was clearly positive. The broader significance lies in what that debut represents. A Korean semiconductor leader has gained a new route into American portfolios and a new platform in the world’s most influential financial market. At the same time, it has stepped more fully into a U.S. conversation that extends far beyond stock performance — one about where the future of chipmaking will happen, which allied companies will shape it and how economic strategy and national security have become inseparable in the semiconductor age.

That makes this more than a listing story. It is a snapshot of how global business works now: capital markets, industrial policy and technological competition all converging in a single ticker symbol. For American investors, SK hynix’s debut offers easier access to one of the world’s key memory-chip makers. For Washington, it is another sign that the future of semiconductors will be written through close — and sometimes uneasy — coordination with Asian allies. And for South Korea, it is evidence that one of its core industrial champions is no longer just participating in the global chip race from afar. It is competing for attention, influence and capital at the center of it.

0 Comments